Given the current macroeconomic climate, it is no surprise that startups and small businesses are left with a laundry list of questions unanswered. How will I raise my subsequent funding round? Where will it come from? What should I be doing to best prepare myself for a potential recession? As an active player in the startup fintech community, Rutter partnered with product leaders at Capchase and Modern Treasury last Thursday to discuss the latest trends within the alternative financing space, and what this means for their borrowers.

The panel cohosted by Rutter & Modern Treasury consisting of Prathik Naidu, Product Lead at Rutter, Sri Muppidi, Product Lead at Capchase, and Ani Narayan, Product Manager at Modern Treasury answered questions delivered by Ben Rathi, Product Marketing Manager at Modern Treasury. In this structured, yet candid, dialogue the panel touched on four specific subtopics within alternative financing.

Revenue-Based Financing: The Future of Small Business Lending

Traditionally, when a small business or startup needs to raise capital, they approach a commercial bank for a business loan. However, the issue here touched on by Ani is that these loans are stringently underwritten with high interest rates and high collateral favoring businesses with extensive credit history. With the explosive growth of ecommerce and startups in the post-pandemic era, alternative lenders like Capchase provided a solution for more founder-friendly funding.

In the revenue-based financing model, commercial borrowers are underwritten by their future revenue streams. This way, early stage founders can access up-front, non-dilutive capital, with no warrants associated, commonly seen in venture debt financing. Typically, Capchase issues these single digit discount rate loans in just 24 hours, creating a new standard in the lending market. In order to meet this underwriting efficiency, real-time access to niche, alternative financial data is needed.

The Importance of Alternative Financial Data

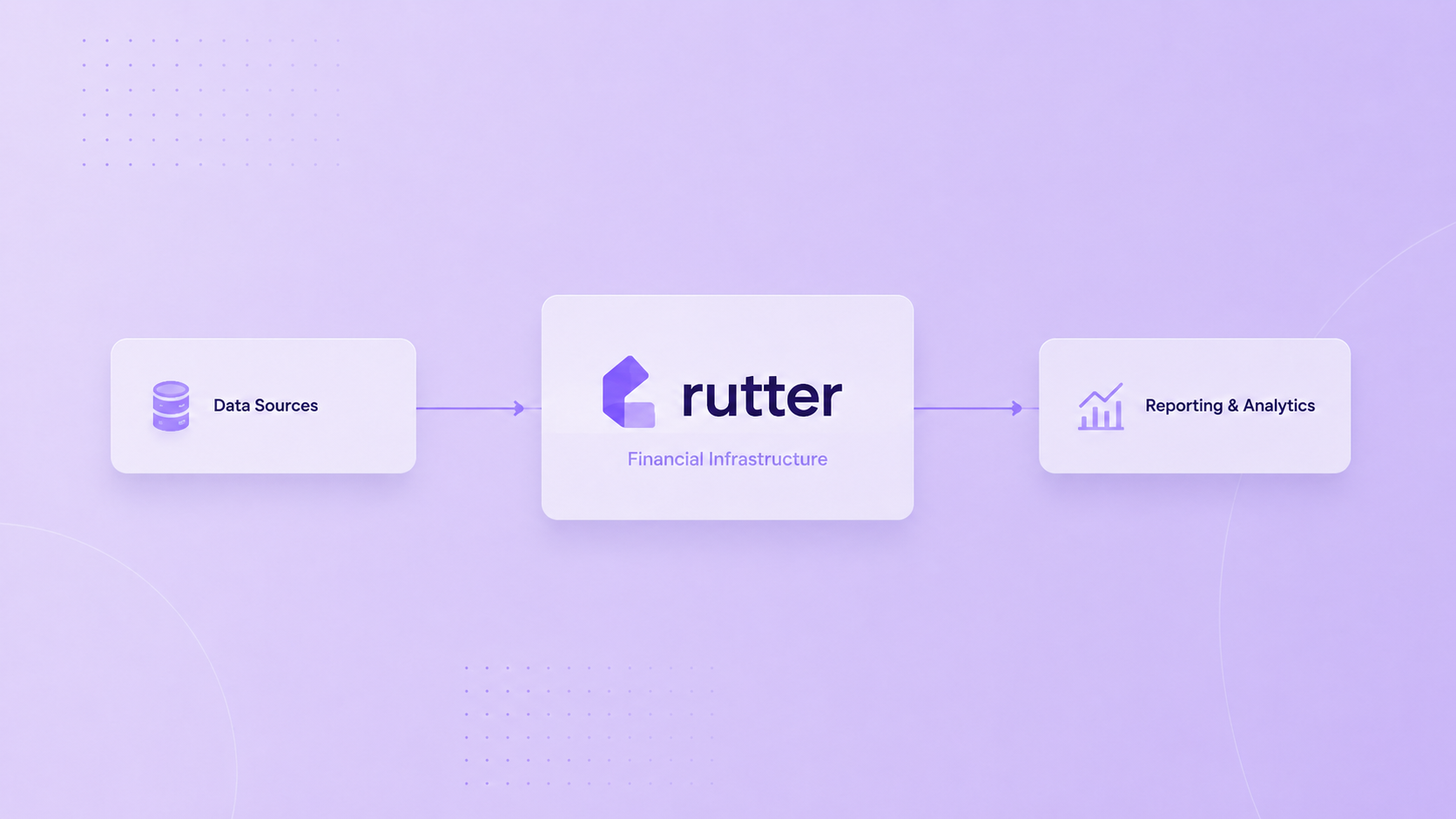

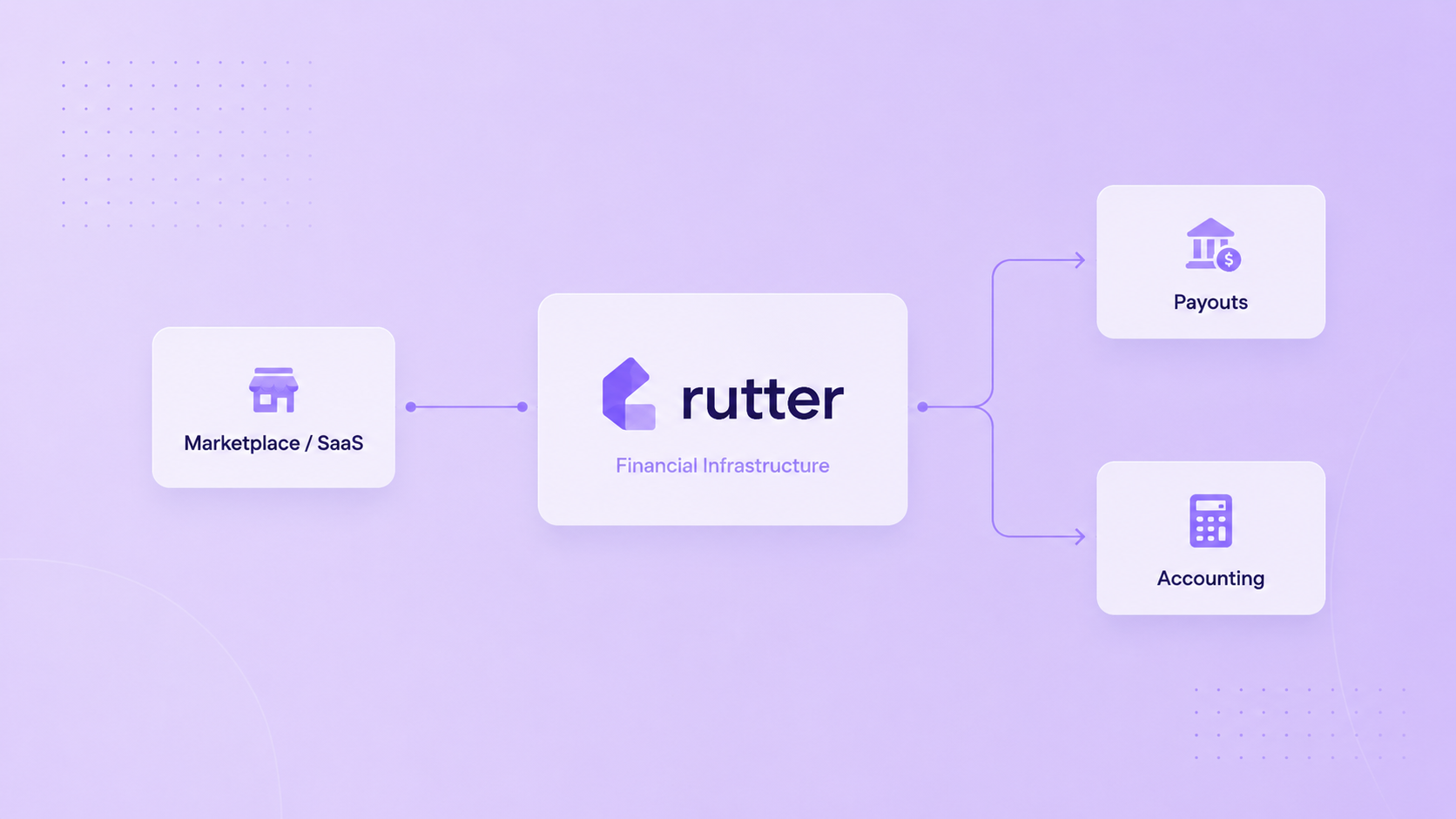

Gone are the days of uploading PDFs of accounting statements, and emailing banking information back and forth. By leveraging universal APIs like Rutter, lenders can access key alternative data points through pre-built integrations to leading commerce and accounting platforms like Shopify, Stripe, QuickBooks, and NetSuite to name just a few. With structured and normalized data coming from several different platforms, underwriting models are enriched with transactional insights, rather than vague banking data.

With access to real-time financial data, lenders are now able to establish a partnership with their borrowers for continued financing, rather than leave clients with a single lump sum. As mentioned by Prathik, alternative data allows lenders to get a far more accurate business financial picture, while providing the best possible experience for the borrower.

Learn more about Rutter’s Universal Commerce API.

The Evolving Financing Tech Stack

With the increase in complexity of underwriting models, a greater demand is placed on a robust technology stack for financing. Described by Ani, at the core of modern underwriting is the financial data that powers the process, so companies like Rutter are critical partners for providing a core commerce and accounting data infrastructure. The second piece is management of payments and operations, and this is where Modern Treasury comes in, allowing companies to automate payments from initiation to reconciliation. In monitoring these transactions on behalf of the customer companies like Modern Treasury also provide out-of-the-box fraud protection, seeking to prevent it before it actually occurs.

The Build vs. Buy Debate

As new players enter the alternative lending space, a key differentiator for companies like Capchase is truly owning the decision making process and getting funding in the hands of founders in 24 hours or less. While the leading alternative lenders rely on integrations to make this experience as seamless as possible, there is still disagreement in building these integrations in-house, or relying on companies like Rutter to build and maintain these integrations on the company’s behalf.

The common misconception is that having an engineering team develop integrations saves the company time and money. However, what they fail to realize are the engineering quirks associated with so many different platforms, like constantly changing APIs, non-standardized data, and ongoing maintenance managing connections. When partnering with a data infrastructure team like Rutter, engineers are freed from building and maintaining these integrations, allowing them to focus their efforts back to building a best-in-class product.

Learn more about how companies should think about the Build vs Buy debate.

Conclusion

Despite many exciting strides being made within the fintech space, it’s still certain that these are scary financial times for everyone. While each panelist represents a different perspective in fintech, Prathik, Ani, and Sri all mentioned the importance of putting the customer at the center of their efforts. Whether it be with critical financial data from Rutter, payments operational efficiency from Modern Treasury, or founder-friendly funding from Capchase, these companies all seek to enable the best experiences for their customers.

We’re building the data infrastructure for commerce. If you’re interested in learning more about how we work with leading companies like Ramp, Mercury, Parafin and more, reach out.