Industry

Financial AI Agents and MCP: How AI Workflows Connect to Systems of Record

Learn how financial AI agents and MCP connect LLM-powered workflows to accounting, ERP, commerce, and payments systems of record for safe read/write automation.

Most small and mid-sized businesses manage their finances using a patchwork of tools. QuickBooks tracks the books, Stripe handles payments, Toast runs point of sale, Gusto processes payroll, and the bank holds the cash. Each system does its job, but none of them work together.

The result is duplication, manual work, and limited visibility. Research shows that nearly 8 out of 10 SMBs juggle multiple systems, and almost all would prefer a single platform to manage finance (BuiltIn).

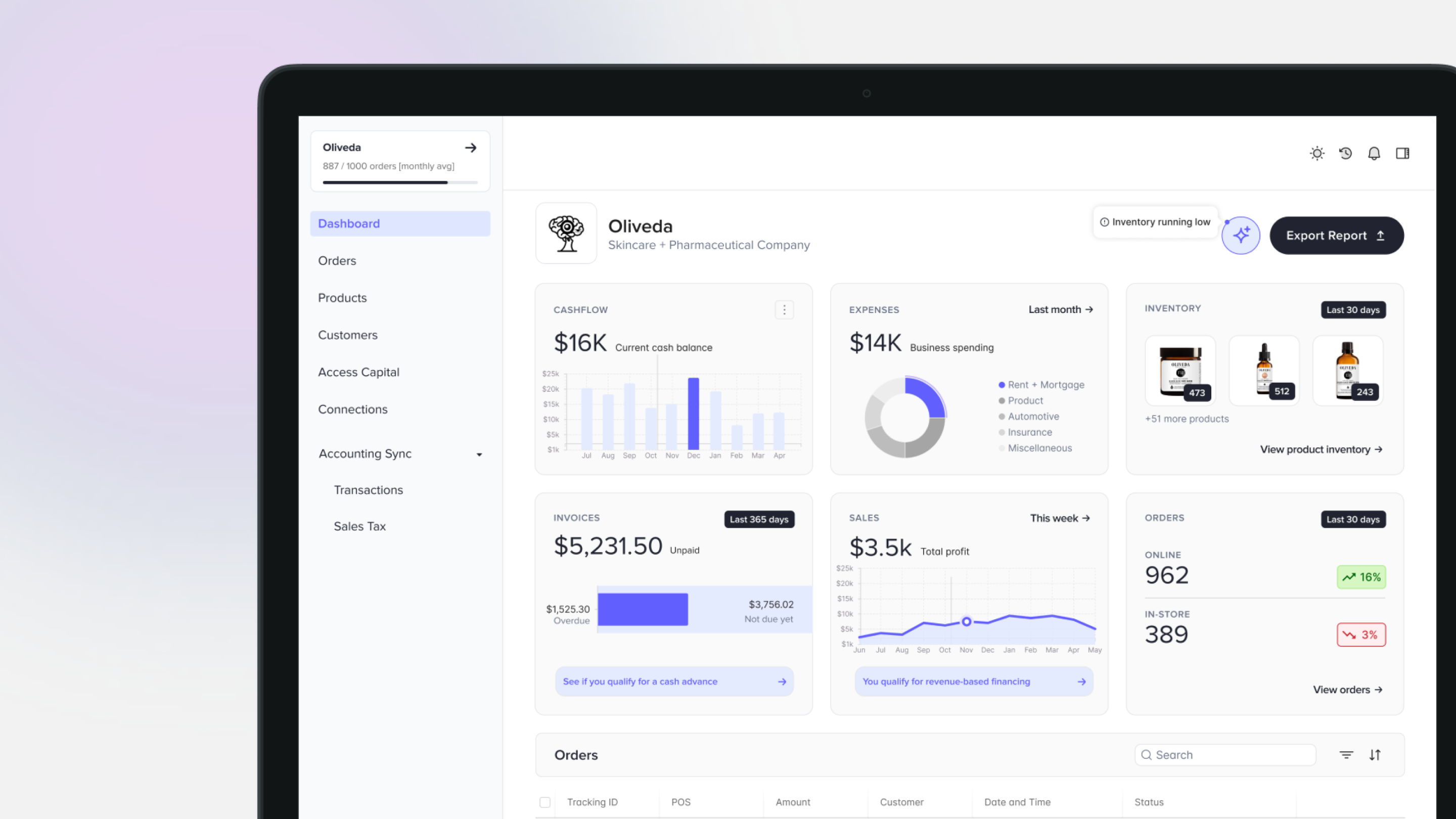

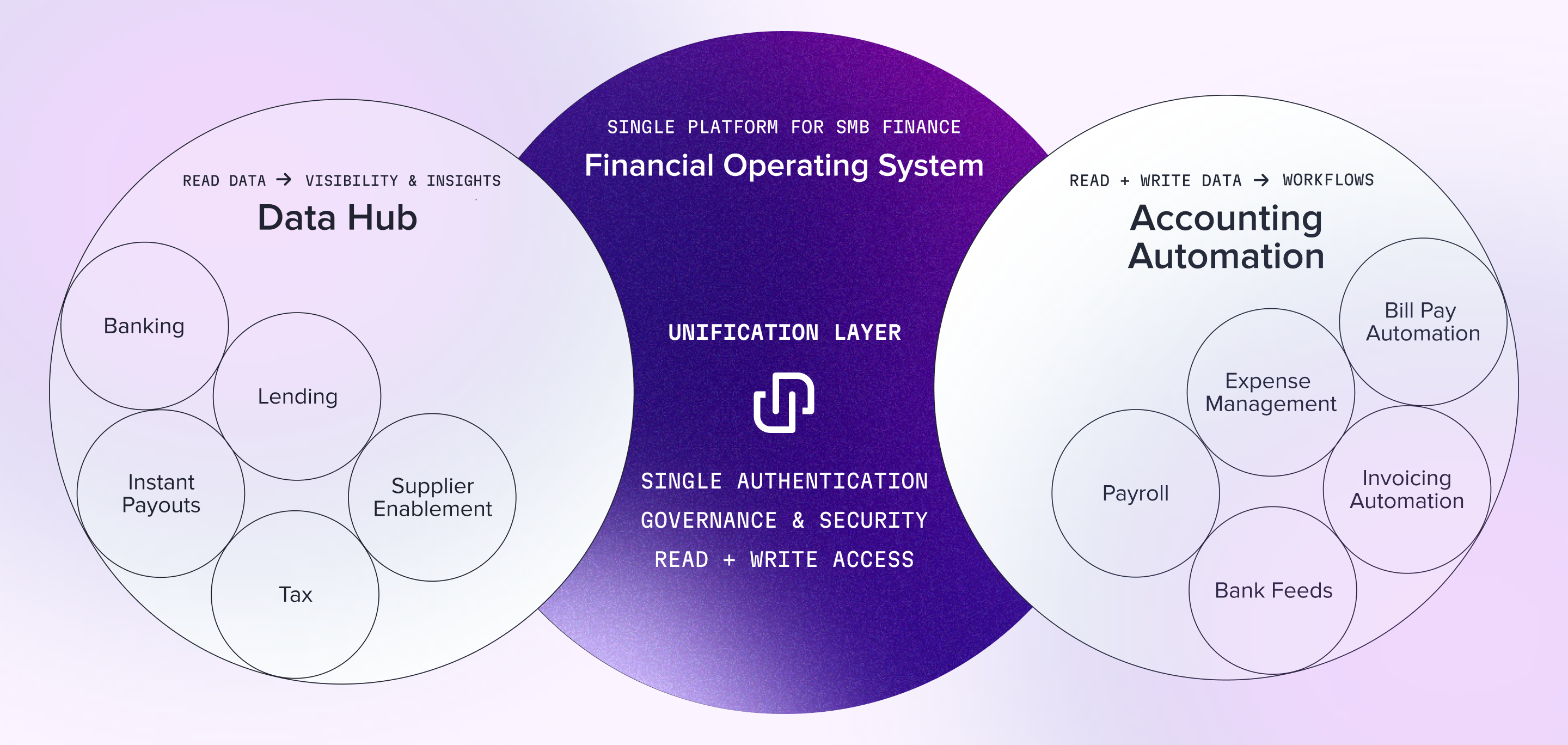

The Financial OS is that platform. Instead of disconnected apps, it provides one place to manage money in, money out, cash flow, insights, and every core financial workflow.

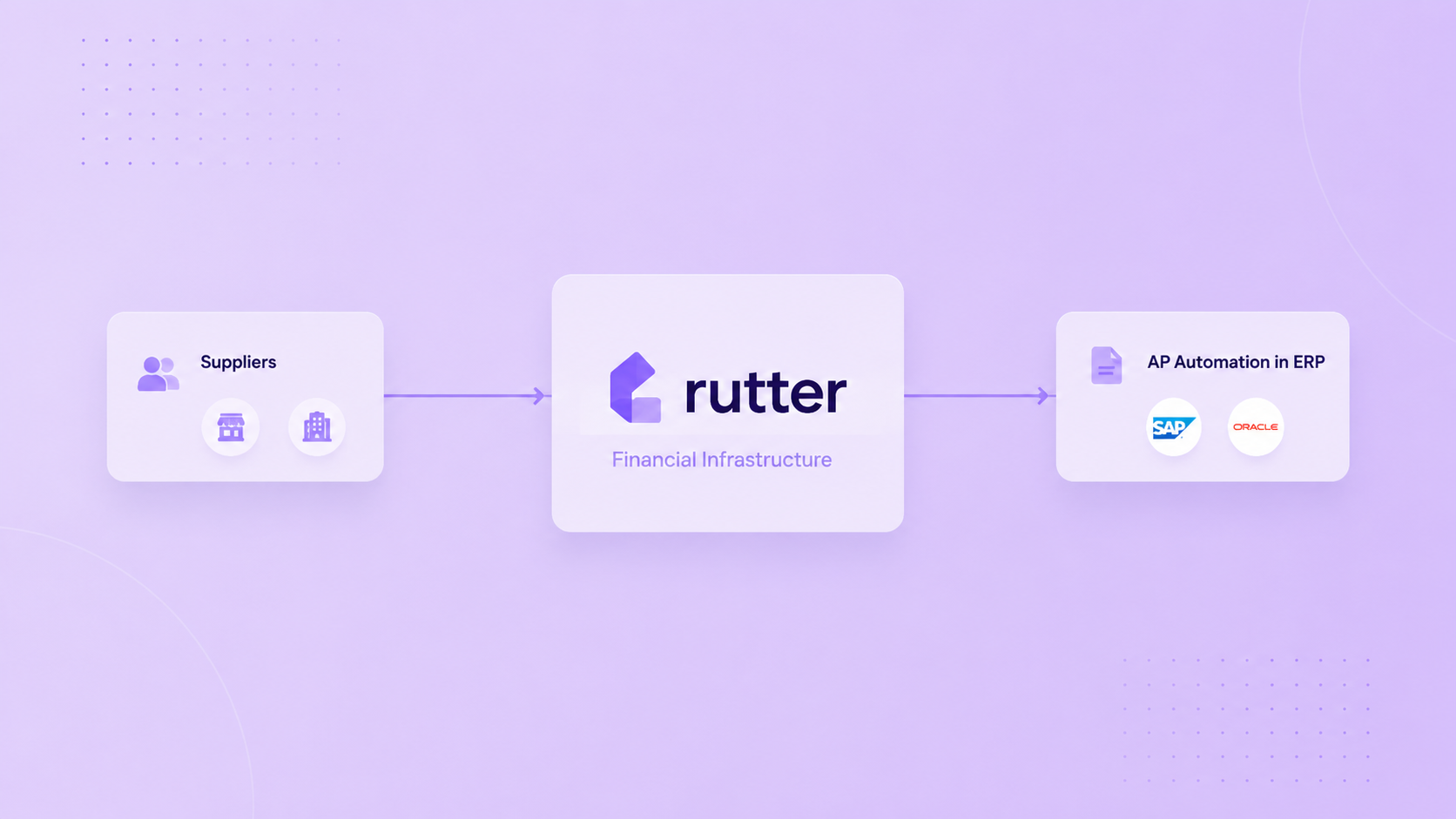

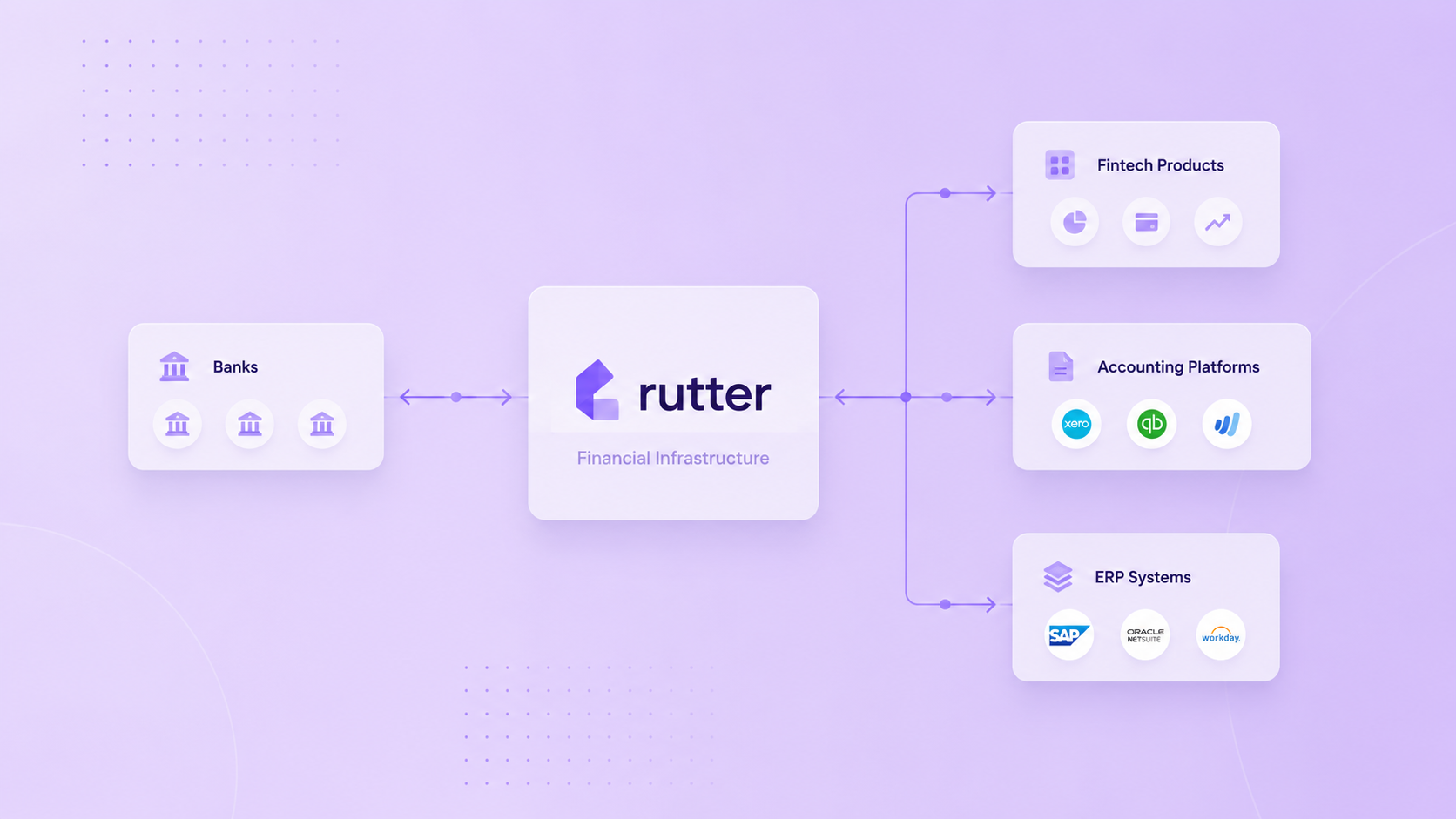

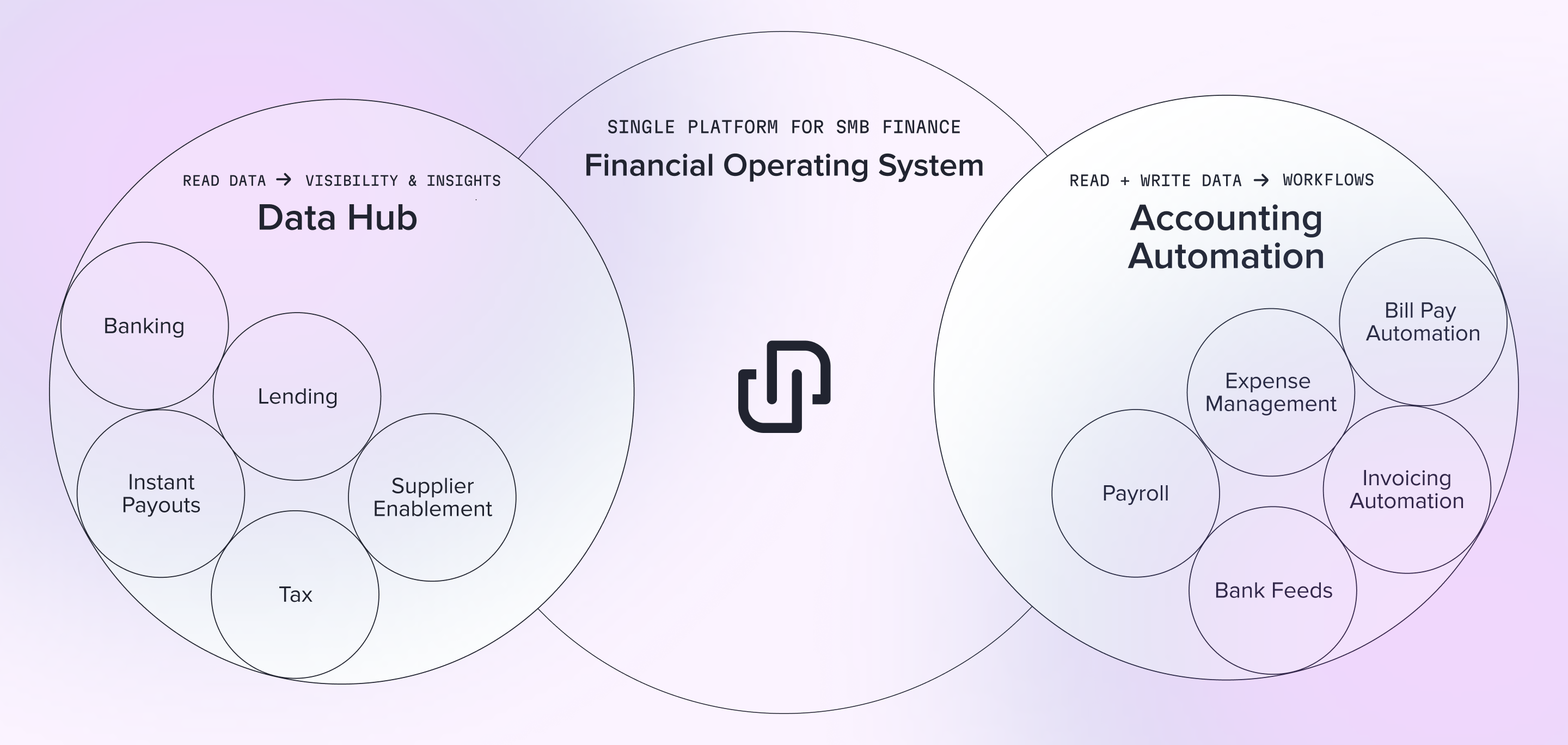

The Financial OS is the single platform for managing all of a company’s financial operations. It brings together money in, money out, cash flow, insights, and daily workflows in one place. Banks, fintechs, and vertical SaaS platforms are building toward this vision. Rutter provides the integrations that power it.

One way to understand the products inside the Financial OS is to group them by how they use data:

Both groups are essential. Data Hub products deliver visibility and intelligence, while Accounting Automation products execute the workflows that keep finance running. Together they form the Financial OS: a single platform for financial operations. The platform is usually delivered by a single vendor such as a bank, fintech, or vertical SaaS provider, but it may also include components from embedded fintech partners. Rutter provides the integration layer that connects these systems, and we partner with embedded fintechs to make the OS complete.

For SMBs, the benefits are straightforward. They save time on manual work, gain real-time visibility into cash flow, and access credit and payments more easily.

For banks and fintechs, the Financial OS is more than a vision. It is a growth strategy. Embedding financial products directly into the workflows that businesses already use drives adoption, deepens retention, and unlocks new revenue.

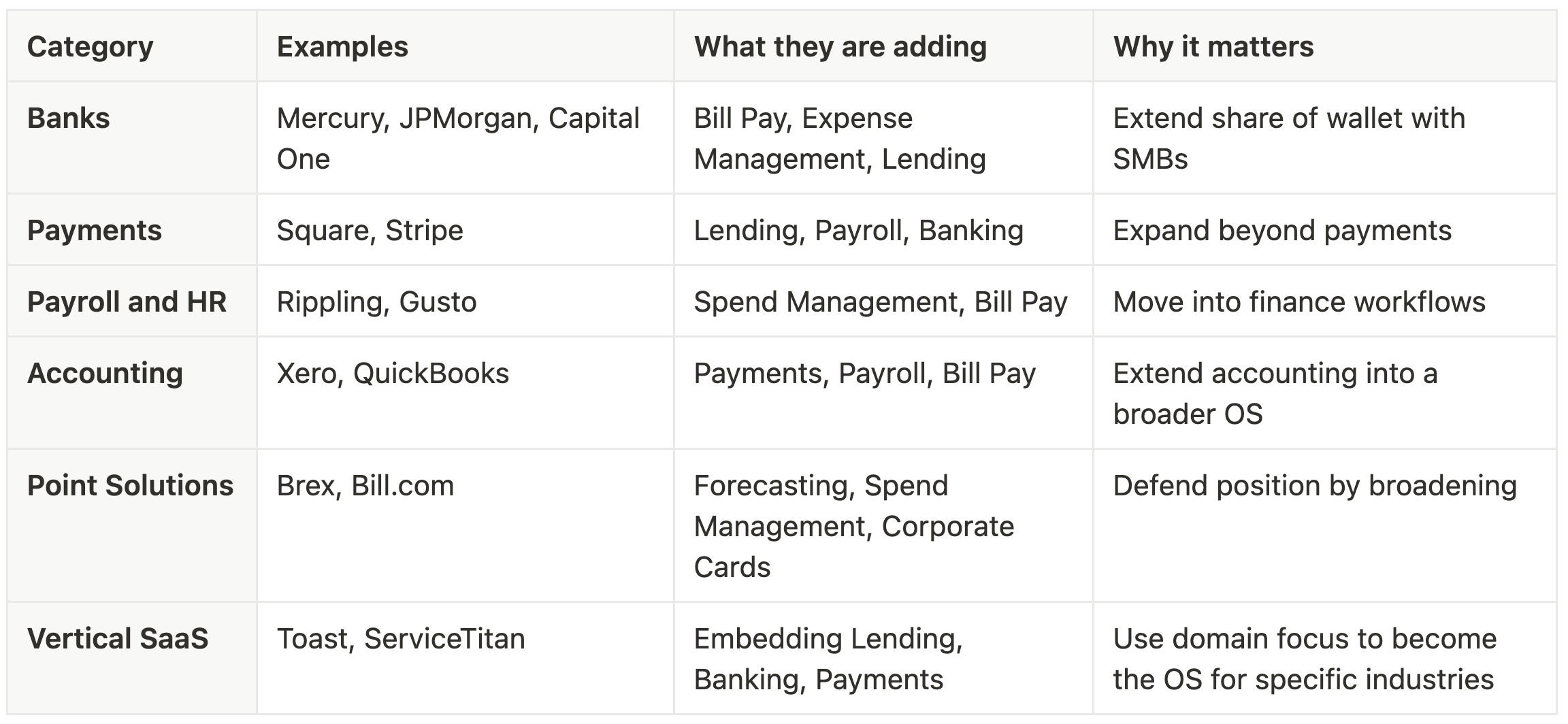

Every major provider is moving beyond its core to offer a broader set of financial products.

The trend is clear. Everyone is chasing the Financial OS. The winners will be those who deliver the best products and the most seamless workflow automation for SMBs.

There is no single path to the Financial OS. Most platforms combine what they build themselves with what they integrate from partners.

Most platforms mix both approaches. A bank might build bill pay in-house, embed lending from a partner, and integrate payroll through APIs.

The Financial OS only works if products can access and act on data from the systems businesses already use: accounting for financials, commerce for sales, banks for cash, and payroll and HR for people and expenses.

A unification layer makes this possible by sitting between those systems of record and Financial OS products. It standardizes connections and provides three core functions:

Without a unification layer, the Financial OS remains an idea. With it, institutions and platforms can deliver a secure, integrated system for financial operations.

The Financial OS is the vision of a single platform where SMBs manage all of their financial operations. Banks, fintechs, and vertical SaaS providers are the ones building and delivering these platforms to their customers. In many cases, they extend their platforms with embedded fintech components like lending, payments, or cards.

Rutter is not building the end-to-end Financial OS. Instead, we provide the integration layer that makes it possible. With one unified API, our customers can connect to accounting, commerce, banking, and payroll systems. We also partner with embedded fintech providers so our customers can plug these capabilities directly into their platforms.

In short, Rutter supplies the connective tissue. We make it faster and easier for our customers to assemble the Financial OS, whether they are embedding third-party components or delivering first-party experiences.

This post introduced the Financial OS vision. Next we will explore Layer 2, the two groupings of products.

From there, we will move into Layer 3, with deep dives into each product use case, along with examples from the market.

Follow along as we publish the rest of this series to stay updated as we cover each layer of the Financial OS.

Building integrated products is hard. We can do that together. Let's chat.