Product

Introducing Rutter Embedded ERP

Rutter Embedded ERP is a new way for fintechs and banks to deliver their products as native experiences inside the ERPs their midmarket customers run on.

Understand the key differences between these integration types and how each one can unlock massive revenue for your business

Your product team is researching how to get your transactions seamlessly imported into your customers’ ERPs. You've been down several rabbit holes. Do you need to integrate with Plaid? The QuickBooks API? The documentation is confusing, the sales calls are contradictory, and you're not even sure you're asking the right questions.

Three months into research, you realize the fundamental issue: there are three completely different types of financial APIs that handle transaction data, but they solve entirely different problems. The naming doesn't help, and most vendors don't clearly explain which category they're actually in.

This scenario plays out constantly in fintech because the financial ecosystem has three distinct categories of APIs that sound similar but solve completely different problems. Understanding the difference isn't just about avoiding wasted research cycles. It determines whether you're building features that drive competitive differentiation or just catching up to table stakes.

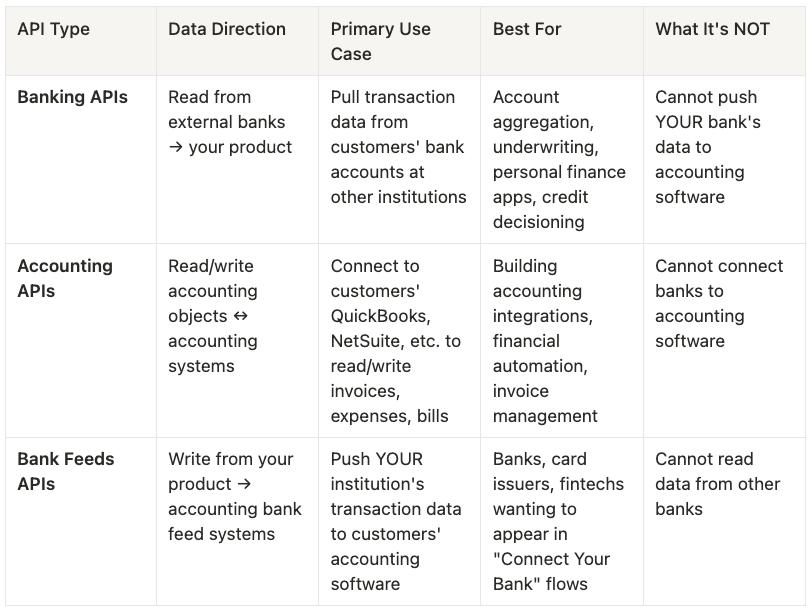

The financial API ecosystem breaks down into three core categories, each with different data flows, use cases, and target customers. What often confuses teams is that all three handle financial transaction data, but in fundamentally different ways.

The key insight is that these APIs solve different parts of the financial data workflow.

Banking APIs pull transaction data from external institutions into your platform. Accounting APIs read and write structured business objects in accounting systems. Bank feeds push your transaction data into accounting systems where your customers can reconcile it.

The data can be quite similar, including fields like transaction amounts, dates, descriptions, merchant information. However, the method to access that data and the business implications of integrating with it are wildly different.

Accounting APIs work with structured business objects like invoices, expenses, bills, and customers. They allow you to fetch, create, and update the formal accounting records that businesses use in their ERPs for financial tracking.

Expense management platforms use accounting APIs to sync categorized expenses into QuickBooks. Invoice automation tools create and track receivables. Financial reporting dashboards pull structured data for analysis. Any workflow that needs to read or write accounting records will make use of this category of APIs.

Accounting APIs don't handle raw bank transactions or reconciliation workflows. Creating expense records in QuickBooks isn't the same as appearing as a bank connection. These are different user experiences and data flows, and provide different value to your customers. (Keep reading to understand how these two workflows can be combined.)

Every accounting platform models data differently. Xero’s invoice line items don’t work like NetSuite’s, and Sage Intacct's project accounting doesn't map to QuickBooks’ project structure. In addition, each API has different auth, rate limits, and validation rules, requiring totally separate builds and consistent maintenance.

To avoid building a dozen different integrations, consider using a unified API like Rutter's Accounting Automation product. Unified APIs provides one API that works across QuickBooks, NetSuite, Sage, Xero, and more, handling all the platform-specific complexity so you don't have to build separate integrations for each accounting system your customers use.

Accounting APIs work with structured business objects like invoices, expenses, bills, and customers. You're creating and updating the formal accounting records that businesses use for reporting and compliance.

Expense management platforms use these to sync categorized expenses into QuickBooks. Invoice automation tools create and track receivables. Financial reporting dashboards pull structured data for analysis. Any workflow that needs to read or write accounting records fits here.

Accounting APIs don't handle raw bank transactions or reconciliation workflows. Creating expense records in QuickBooks isn't the same as appearing as a bank connection. These are different user experiences and data flows entirely.

Every accounting platform models data differently. QuickBooks multi-currency works nothing like NetSuite. Sage Intacct's project accounting doesn't map to Xero's structure. Each has different auth, rate limits, and validation rules. You end up building 4+ separate integrations.

Rutter's Accounting Automation provides one API that works across QuickBooks, NetSuite, Sage, Xero, and more. We handle all the platform-specific complexity so you don't have to build separate integrations for each accounting system.

Bank feeds get your financial institution appear as a listed bank in accounting software. Your customers search for your bank in QuickBooks, connect to it like they would for Chase or Wells Fargo, and get your transactions automatically synced into the ERP for reconciliation.

Any financial institution that wants to eliminate CSV downloads and manual imports for their business customers needs bank feeds. You don’t need to be a traditional bank to get listed—if you offer a banking or card product to your customers, your customers would benefit from bank feeds. Neobanks use these to get their transactions into customer ERPs just like their customers get at traditional banks. Corporate card companies use this to offer seamless reconciliation.

Bank feeds can’t pull data from other banks or create structured accounting records. They only push your institution's transaction data into specialized reconciliation systems within accounting platforms.

Most accounting platforms restrict bank feeds to certified financial partners. Intuit requires extensive partnerships and compliance verification. The process takes 12+ months, which kills momentum for smaller banks and emerging fintechs who can't wait that long.

As an alternative, Rutter's Bank Feeds product leverages our existing partnerships with accounting platforms. Instead of building relationships with Intuit, Sage, and Xero separately, you use our established connections and our unified API infrastructure. Instead of the normal year-long process for each ERP you want to support, we get you listed and live across 10+ platforms in 2-4 weeks.

Most financial institutions eventually need some combination of all three API types, but for different use cases and customer segments.

Consider a corporate card issuer. They need bank feeds so their transactions appear automatically in customer accounting systems for reconciliation. They might also need banking APIs to pull data from customers' other bank accounts for underwriting or credit limit decisions. And they could use accounting APIs to create detailed expense categorization or integrate with specific accounting workflows.

The key is understanding which API type drives the core customer value proposition. For most financial institutions serving business customers, bank feeds create the stickiest competitive advantage because they eliminate manual reconciliation work that customers hate.

Mercury, the neobank targeting startups and SMBs, has built significant competitive advantages through both superior banking features and seamless accounting integrations. When a startup's CFO evaluates Mercury against traditional business banks, Mercury wins on multiple fronts: better user experience, competitive rates, and superior back-office automation.

The accounting integration piece is particularly compelling. Mercury transactions automatically appear in QuickBooks within hours through bank feeds, while traditional banks typically require monthly CSV downloads and manual reconciliation. This isn't a nice-to-have feature. It's a fundamental workflow efficiency that saves finance teams hours every month, and a core requirement that comes up over and over again in banking RFPs.

Financial institutions often underestimate how multiple integration approaches can work together. Banking APIs can enhance underwriting and customer insights. Accounting APIs can power specialized workflow automation. Bank feeds can eliminate reconciliation friction. The combinations create compound competitive advantages.

The technical requirements vary significantly across API types. Banking APIs focus on handling authentication with external institutions, managing data refresh cycles, and dealing with connection reliability issues. Implementation typically takes 4-16 weeks depending on the number of aggregators you need to support.

Accounting APIs require mapping between your data model and multiple accounting platforms, handling platform-specific authentication methods, and managing sync reliability across different systems. Implementation can take 12-20 weeks for comprehensive coverage.

Bank feeds require partnership agreements with accounting platforms plus technical integration with their reconciliation infrastructure. Direct implementation can take 12+ months due to partnership timelines and compliance requirements. Working with an existing partner like Rutter reduces this to 2-4 weeks.

For financial institutions evaluating their integration strategy, the question isn't which API type to choose. It's understanding which combinations will drive customer acquisition and retention in your specific market segments.

The financial institutions winning corporate banking deals aren't necessarily those with the best banking features. They're the ones that integrate seamlessly into existing business workflows and meet customers in the tools they’re already using. Bank feeds create that integration by eliminating the manual reconciliation work that every business customer deals with monthly.

Regional banks lose commercial customers to digital-first institutions not because of interest rates or account features, but because competitors offer seamless accounting integrations that save customers hours of administrative work every month.

Rutter's approach addresses this complexity by offering all three integration types through unified products: Smart Banking for external data aggregation, Accounting Automation for business object integration, and Bank Feeds for reconciliation workflows. Financial institutions can implement the right combination for their customers without managing multiple vendor relationships or technical integrations.

Ready to understand which integration strategy fits your customer needs?

Get started with Rutter's unified financial API platform

Building integrated products is hard. We can do that together. Let's chat.