Industry

Financial AI Agents and MCP: How AI Workflows Connect to Systems of Record

Learn how financial AI agents and MCP connect LLM-powered workflows to accounting, ERP, commerce, and payments systems of record for safe read/write automation.

If you're building a B2B fintech product and need accounting, commerce, or ERP integrations, you've probably looked at Codat, Merge, and Rutter. All three are unified API providers. All three reduce the pain of integrating with systems like QuickBooks, Xero, NetSuite, Shopify, and Stripe. But they are not interchangeable, and choosing the wrong one can create months of integration debt, workflow compromises, and future re-platforming.

This guide is designed to help product, engineering, and partnerships teams answer a simple question: which unified API is the right fit for your product today, and which one will still make sense as your roadmap expands?

The most useful way to compare these companies is not by looking at their homepages or feature lists in isolation. The real distinction comes down to what kind of customer they are built for, how deep they go within financial workflows, how they handle read and write operations, and how much implementation support they provide when the edge cases start to matter.

The biggest difference between these providers is not that one has APIs and the others do not. The deeper difference is what kind of customer and workflow each company has chosen to optimize around.

Codat began with strong momentum around SMB accounting data and lending-adjacent use cases. Over time, its positioning expanded into spend intelligence, supplier enablement, and related bank and issuer workflows. That can make it compelling for organizations whose product strategy begins with financial data access and extends into card or supplier programs.

Merge is built around horizontal breadth. Its value proposition is straightforward: one unified API platform that can cover accounting, HRIS, ATS, CRM, ticketing, file storage, and other categories. That breadth is useful for software companies that want a single vendor across many types of integrations. The tradeoff is that a broad horizontal platform is not always the same thing as a provider designed around the operational realities of B2B fintech products.

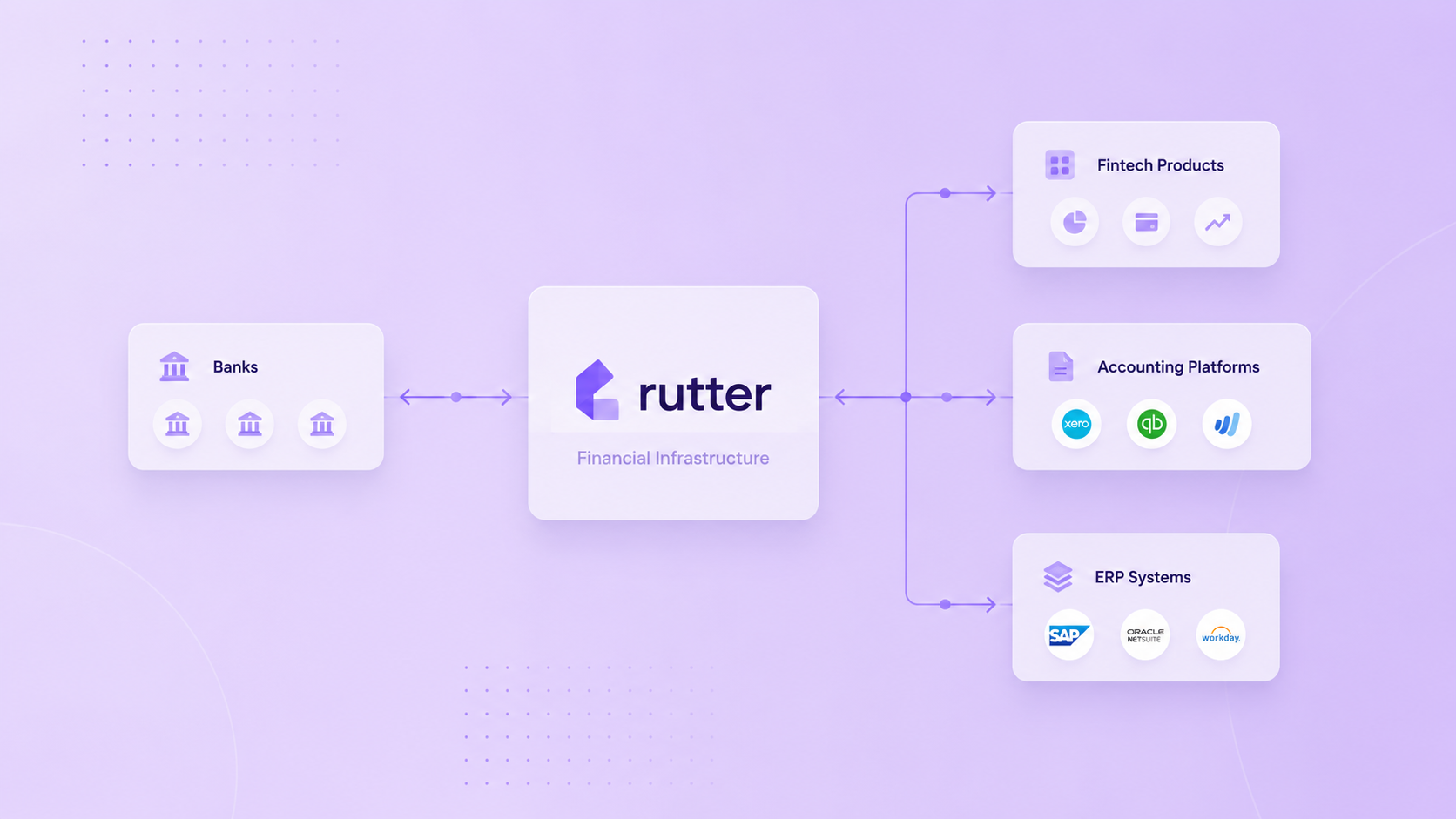

Rutter is purpose-built for B2B financial products. The platform is oriented around accounting, commerce, payments, and the workflows that depend on them: underwriting, reconciliation, invoice automation, expense syncing, bank feeds, and embedded finance. If your product roadmap is moving toward a financial operating system model, that orientation matters.

Most comparison pages start with a list of logos. That is not enough. In practice, teams should care about endpoint depth, object coverage, write support, and how much one provider can reduce cross-system complexity inside the product.

All three providers can cover major systems such as QuickBooks Online, Xero, and NetSuite in some form. The more important question is what you actually need to do inside those systems. Reading summary data for underwriting is one level of difficulty. Writing bills, invoices, payments, journal entries, or item-level updates into a system of record is another.

If your workflow combines multiple domains, such as commerce data for underwriting plus accounting sync for ongoing reconciliation, integration strategy becomes even more important. Using multiple vendors or mixing in-house builds can work, but it often introduces fragmented authentication, inconsistent schemas, and additional maintenance. Unified APIs create the most value when they eliminate that fragmentation rather than merely hiding it.

Teams evaluating unified APIs should also look closely at data architecture. Some providers primarily act as a passthrough to the source system, while others maintain normalized data that can be queried more consistently. The right model depends on your use case, but the architectural choice affects latency, rate-limit exposure, historical access patterns, and how resilient your product is when upstream systems slow down.

For fintech products, this is not just an infrastructure detail. It shapes customer experience. Faster fetches improve onboarding and underwriting. Better normalization reduces engineering complexity. More reliable sync patterns reduce support tickets and manual intervention.

Write accounting is where many fintech teams discover the difference between a connector and a product infrastructure layer. Reading data is relatively straightforward compared with writing into a financial system of record correctly.

Accounting systems are opinionated. Tax treatment, currency handling, contacts, line items, account mappings, posting rules, and object relationships all matter. A technically successful API request can still create bad accounting if the workflow is not designed carefully.

That is why write quality should be treated as a product capability, not a checklist item. When you evaluate a provider, ask how they handle idempotency, validation, sync reliability, asynchronous versus immediate write patterns, observability, and implementation guidance. Ask how they support edge cases. Ask what happens when a customer has a messy chart of accounts, region-specific tax rules, or a nonstandard workflow that still has to reconcile cleanly.

At the enterprise level, support is part of the product. A unified API can look strong in documentation and still fail during implementation if the vendor cannot guide architecture, UX choices, and go-to-market sequencing.

The best support models usually include hands-on solution design, clear escalation paths, implementation working sessions, and guidance around how end users will authenticate, map data, and recover from errors. This becomes especially important when engineering, product, partnerships, and finance teams all need to align around one workflow.

If your team expects to launch quickly, expand into new workflows, and avoid expensive rework later, the implementation model should be part of the buying decision from the start.

The simplest way to choose is to start from the product you are actually building rather than the provider category you think you need.

If you are building around supplier enablement, spend visibility, or bank-led SMB data use cases, Codat may be the best fit to evaluate first.

If you need a broad unified API layer that reaches well beyond finance into HR, recruiting, CRM, support, and file systems, Merge will often be the most efficient option.

If you are building a B2B fintech product where accounting, commerce, payments, reconciliation, underwriting, invoice automation, or bank-feed style workflows sit near the center of the roadmap, Rutter is usually the strongest strategic fit.

The wrong question is, 'Which provider has the most connectors?' The better question is, 'Which provider most closely matches the product architecture and workflow complexity we expect to support over the next two years?'

There is no single best unified API for every software company. There is a best fit for the product category you are building.

For generalized integration breadth across many software categories, Merge is hard to ignore.

For SMB financial data, supplier-oriented workflows, and bank-adjacent use cases, Codat can be a strong option.

For B2B fintech teams that need deeper accounting and financial workflow support, plus a platform designed around how financial products actually operate, Rutter is the most compelling choice.

If your roadmap is heading toward a more connected financial product suite, where commerce, accounting, payments, and operational workflows increasingly need to work together, picking a finance-native integration partner early can save a meaningful amount of rework later.

Building integrated products is hard. We can do that together. Let's chat.