.png)

Industry

How to Design an Approval Matrix for ERP-Native Payments

Build an approval matrix for ERP-native payments using roles, thresholds, entities, risk conditions, escalation, and audit evidence.

Payments products tend to be evaluated by the moment money moves. Did the ACH debit initiate? Did the wire send? Did the card transaction clear? Did the payout settle? But the customer experience is shaped by everything around that moment: where the payment is initiated, how the account context is selected, how the ledger updates, how reconciliation happens, and whether the workflow fits inside the customer's existing operating system.

That is why payments and money movement APIs are becoming part of a broader product infrastructure stack. A bank, card issuer, payment processor, or B2B fintech might already own its rails. The harder question is how to embed those rails into the customer's financial workflow without forcing the customer into a separate portal.

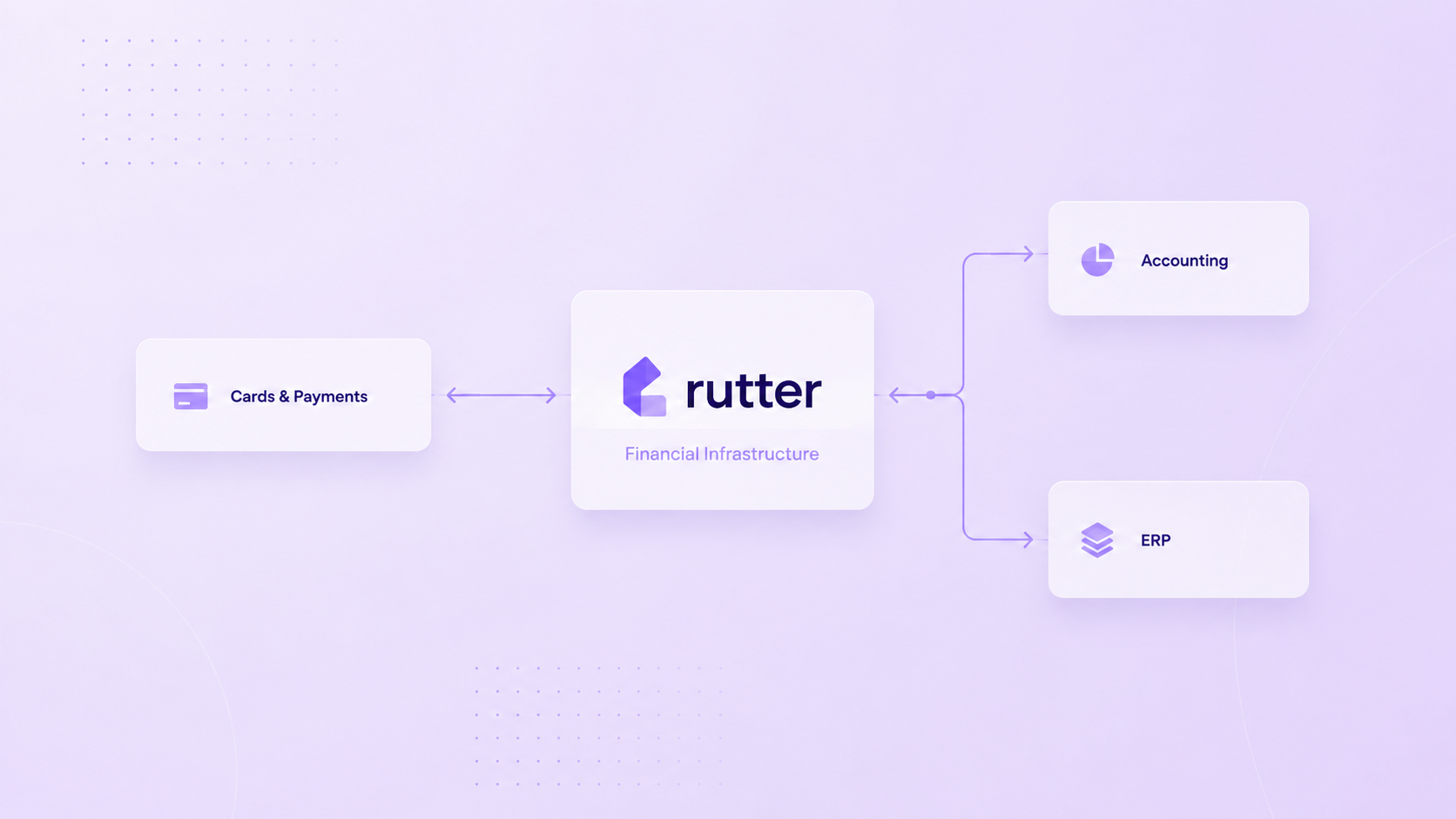

Rutter’s Payments API helps product teams read payments, transactions, subscriptions, balances, and payouts. Rutter’s Accounting API and embedded products help those movements connect back to accounting systems and ERPs. Together, they support a rails-neutral model: the fintech or bank keeps its payment infrastructure while Rutter connects the workflow to the systems where customers operate.

A payments and money movement API gives a product access to the data and workflows surrounding transfers, transactions, payouts, settlements, and payment records. Depending on the product, the API may read payment data, initiate money movement through a customer's rails, or reconcile payment activity back into accounting and ERP systems.

In B2B fintech, the most useful payments API is rarely just a single endpoint. It usually has to support:

A money movement product has to work across multiple moments. It starts before the payment, when the customer chooses what to pay and which rail to use. It continues during execution, when the payment moves through the bank, processor, or sponsor-bank infrastructure. It ends only after the customer's books reflect what happened.

Rails-neutral means the product infrastructure does not force a bank or fintech to replace its payment rails. A regional bank may already have core banking infrastructure, ACH operations, card programs, wires, and business banking relationships. A payments company may already own global payout rails. A fintech may already operate through a sponsor bank. Requiring those companies to change rails just to add embedded workflows creates unnecessary friction.

Rutter’s positioning is built around a different division of labor. The customer brings the financial product, rails, brand, and banking relationships. Rutter brings the integration layer, embedded UI where needed, data normalization, workflow automation, authentication, and observability. That means the money movement layer can stay exactly where it belongs while the product becomes more integrated into the customer’s accounting or ERP environment.

This distinction is especially important for embedded finance. Rutter’s post on where embedded finance products live makes the point directly: integrations are not enough. The product has to show up in the right place. For SMBs, that may be the fintech or bank's digital product. For mid-market businesses, that may be NetSuite, Dynamics, Sage Intacct, SAP, or Workday.

A payments workflow has two jobs. The first is execution. The second is accounting truth.

Execution answers questions like:

Accounting truth answers different questions:

A payments API can solve the first job and leave the customer with the second. For B2B products, that is not enough. Finance teams care about close readiness. Product teams care about adoption. Operations teams care about support volume. All three improve when money movement is connected to the ledger.

Rutter’s bank feeds infrastructure is one example of this accounting truth layer. Bank feeds deliver transaction data into the customer's accounting system or ERP for reconciliation. The product may be a bank account, card program, or payment processor, but the customer experiences the value when transactions land cleanly where the books are closed.

SMB financial products often live in digital apps. A business may log into a bank, spend platform, or payment processor to run payouts, bill pay, expenses, or cash flow workflows. The system of record still matters, but the interface belongs to the fintech or bank.

Mid-market products are different. Finance teams often run AP, treasury, reconciliation, and approvals directly inside the ERP. They may use multiple banks and payment providers. For a single bill, they might choose a payment rail based on bank relationship, currency, timing, FX rate, or cost. That decision belongs inside the ERP workflow, not in a separate app.

Rutter’s Financial OS for midmarket ERP explains why the Financial OS moves into the ERP as customers scale. A payments product that was valuable as an SMB banking app can become less sticky when the customer grows into NetSuite or Dynamics. Embedded payments are not only about adding another integration. They are about keeping the financial product present at the moment of work.

When evaluating payments and money movement infrastructure, product teams should ask more than "can we move money?" The better questions are:

A payments product that only solves one workflow can be useful. A payments product connected to accounting, commerce, ERP, and observability infrastructure can become part of the customer's operating system.

Rutter supports rails-neutral payments and money movement products across several layers.

Rutter APIs connect product teams to accounting, ERP, commerce, payments, and other systems of record. A payments company can read transactions, payouts, and commerce data while also writing accounting records back where needed.

Rutter Embedded ERP lets banks and fintechs surface their payment functionality natively inside ERPs. For example, an embedded FX or cross-border payment workflow can live inside NetSuite while still using the fintech’s own rate engine, trade execution API, and rails.

Rutter Embedded Digital gives banks and fintechs a white-labeled digital surface for SMBs. This is useful when the customer works inside the bank or fintech product rather than inside a mid-market ERP.

Rutter Monitoring gives teams visibility into request logs, webhook logs, data sync history, and connection health. Money movement products need that operational layer because payment and accounting data must stay consistent across systems.

A payments and money movement API helps a product access payment, transaction, balance, payout, and settlement data. In B2B fintech, it often also connects money movement to accounting and ERP systems for reconciliation.

Rails-neutral means the product can work with the bank or fintech's existing ACH, wire, card, sponsor bank, processor, or proprietary rails. The infrastructure adds connectivity and embedded workflows without replacing the financial rails.

Business payments create accounting events. Without accounting integrations, customers often have to reconcile payments manually in their ERP or accounting system.

Rutter provides the integration and product layer around existing rails. It can connect to accounting and ERP systems, support embedded digital or ERP-native experiences, and help teams monitor the health of financial integrations.

Payments are valuable because they move money. Embedded payments are valuable because they move money without moving the customer out of their workflow. A rails-neutral product can preserve the bank or fintech's infrastructure while becoming more useful inside the customer's app, accounting system, or ERP.

For product teams, that is the strategic shift. Building a payments feature is not the same as building money movement infrastructure. The durable product is the one that knows where the customer works, keeps the ledger accurate, and lets the bank or fintech keep the rails it already owns.

Building integrated products is hard. We can do that together. Let's chat.

.png)

.png)