.png)

Industry

ERP Integration for Banks and Fintechs: API, Bank Feeds, or Embedded App?

Compare accounting APIs, bank feeds, and embedded ERP apps by workflow, customer segment, data direction, and implementation burden.

In the current fintech landscape, increasing "share of wallet" isn't just a vanity metric—it’s a direct lever for revenue. For financial institutions and commercial card issuers, calculating the Return on Investment (ROI) of migrating customers to card payments is top of mind.

However, this isn't a simple "plug-and-play" formula. It’s a complex calculation that balances customer-base demographics, Total Payment Volume (TPV), and fluctuating interchange rates.

To help you navigate this complexity, we’ve broken down the three critical steps to estimating your card program's true potential.

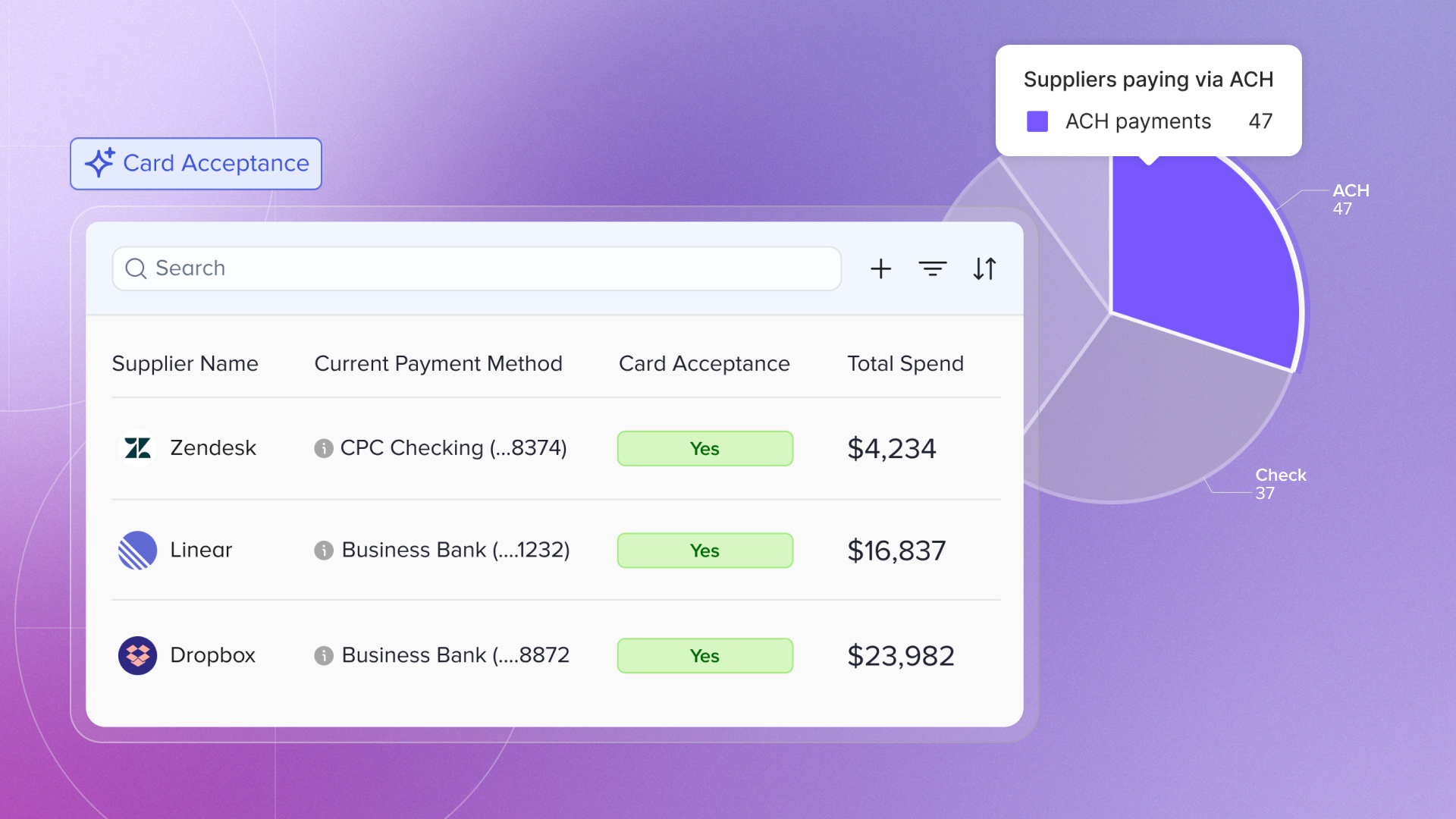

The first hurdle is estimating what percentage of your customer base actually pays vendors willing to accept cards. This number fluctuates wildly based on industry.

According to recent industry data, commercial credit card spending is seeing a significant shift as businesses look to capture rewards and float, with over 50% of businesses using credit cards as a source of funding. At Rutter, we typically see in our customer portfolio that for SMBs, roughly 40-60% of their vendors already accept card payments or are currently being paid via card. As a commercial card division or fintech offering card issuing, there is now significantly more spend to capture than before.

Most issuers rely on first-party data from their own transaction data or the standard Visa/Mastercard APIs. While useful, these often return a mix of "High," "Medium," and "Low" match rates. In our experience, results below a "High" match rate tend to be false positives due to a simple matching process based on vendor name or incomplete address data. We previously published a guide on how to use higher quality signal to determine vendor acceptance.

As a result, we generally see companies starting at different points in terms of their ability to determine vendor card acceptance.

By nearly tripling the identification rate, we provide 2-3x additional leads and opportunities to convert ACH spend into high-margin card spend. This is beneficial for sales teams and customer-facing functions to evaluate the ROI for a prospect, and how much cash back they can deliver as part of their card program.

Once you’ve identified the opportunities, how much of that spend can you actually capture?

Currently, many fintechs only own 20-30% of their customers' card payment volume. The remainder is often "leaking" to legacy corporate cards, being run through low-interchange debit cards, or tied to ACH/wire payment methods.

Total migration is rarely instant; users often hesitate to move all spend at once, or low-priority spend is left unconverted. However, strategic prioritization changes the game. By identifying and targeting high-value vendors—ad spend such as Google Ads, Meta or hosting/SaaS spend like AWS, or Microsoft—you can capture the highest volume first.

With Rutter, by identifying more card accepting vendors and converting the highest volume spend to card, banks and card issuers are seeing their share of wallet increase to 40-50% on average for their clients’ card spend**.** This can translate to more than double the card spend volume compared to the previous state.

For example, if you're doing $100M in vendor payments today just through card, the potential new volume would be ~$190M. This additional $90M in card spend assuming 1.5% take rate on interchange would lead to an additional ~$1.4M in revenue.

Commercial cards are one of the most profitable products in a fintech’s arsenal, but only if you can accurately identify and capture the volume.

The math is simple: better vendor identification leads to higher share of wallet, which leads to increased interchange revenue. According to market metrics, the average small business credit card limit and spend are rising, making the competition for that spend fiercer than ever.

You shouldn't have to guess your revenue potential. If you’re ready to see the real numbers, reach out for a demo today. We’ll take your specific TPV and customer data to provide a comprehensive ROI report, showing exactly how much additional revenue you could be earning with Rutter. Book a demo with Rutter today.

Building integrated products is hard. We can do that together. Let's chat.

.png)

.png)